Banks will need to develop new models in the key product and advisory services sectors if they are to meet the competition posed by the rapid pace of digitalization.

The banking industry’s traditional payment, financing and investment structures are already being undermined by alternative service providers like Paypal or Apple Pay, crowdlending platforms and intelligent robo-advisers.

Microsoft founder Bill Gates’ provocative prophecy almost a quarter of a century ago that «banking is necessary, banks are not» is starting to look ominously true.

Rapid technological advances, and shifts in client demands have seen the development of a Fintech sector whose platforms are now able to offer much cheaper, more user friendly and intelligent products in the banks’ key business areas.

Banks will have to adapt

According to a study by the Zurich-based financial consultants IFBC, banks will have to adapt to increasing digitalization, or die.

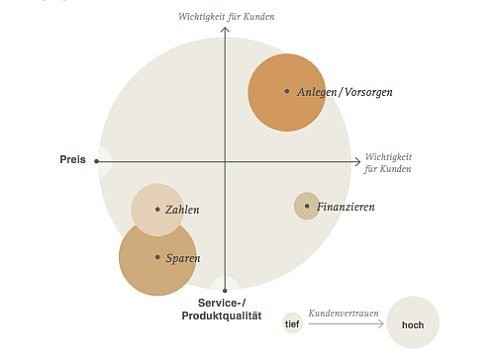

Of the bank’s traditional hegemony, only the savings sector is seen as relatively secure, while the payments system, personal finance, investment and pensions businesses will come under increasing threat from alternative providers, IFBC predicts.

Payments and financing functions can be more easily replaced by alternative providers since price and service quality, rather than client trust, will drive customer choice.

Impact from artificial intelligence

As far as the investment sector is concerned, IFBC sees increasing pressure on traditional banks from further innovations, like for example the impact from artificial intelligence.

In order to compete on price, banks will need to better leverage their scale of size in all areas and adapt their business models to achieve product or advisory leadership.

Leadership on the product side will need to focus particularly on price-performance ratios, and products for the mass-client market need to be transparent and more user-friendly, according to the study.

Focus on clients

Internal processes need to be more efficient to generate lower pricing, and sales channels need to be expanded to reach a broader customer base. Some banks may even need to consider outsourcing certain transaction management and support functions in order to reduce their costs.

To achieve advisory leadership banks will need to focus more on independent and tailor-made solutions for clients rather than in-house product offerings. Unlike the price pressures in the product sector, banks should be able to achieve higher margins in the advisory services, it says.