Citigroup is feting itself as the world's best private bank – and isn't scared of dinging its competition in Switzerland. A finews.com comparison.

The award is considered the gold standard of private banking: the annual «Global Private Banking Awards» hosted by the «Financial Times». This year saw a changing of the guard, with U.S. bank Citigroup snatching the crown as best global private bank from Switzerland's UBS.

Citi's private bank head Peter Charrington concluded on «FT» website«Private Wealth Management» that the reasons behind the U.S. bank's win are that American firms are upsetting the old aristocratic hierarchy of private banking, which is led by Switzerland.

Charrington detailed a series of reasons and evidence to back up his theory – except some of his comments on Swiss banks are imprecise and partly even false.

Wrong Perception of UBS

U.S. private banks emerged strongest from the financial crisis, according to Charrington. He argued that Citi differs from UBS, which doesn't run its wealth management arm as an individual division, but has lumped it together with asset management or retail banking, much like other competitors.

Citi, by contrast, has carved out its private bank as a unit with a strong focus on a demanding wealthy clientele and family offices which want to tap capital market services. This way, Citi can grant its wealthy clients access to institutional trading or advice for foreign exchange trading. «I can’t think of any competitors where their organizational model can deliver that,» Charrington said.

Not the First Time

A glance at UBS' set-up and business model quickly takes the heft out of Charrington's comments. UBS has of course split out its wealth arm as a separate division, and ultra-wealthy clients are given a direct line to investment banking services (like Credit Suisse incidentally as well).

It isn't the first time that a high-ranking Citi private banker has dinged Swiss banks. The New York-based bank's ex-boss in Asia,Bassam Salem, said three years ago that Swiss firms in particular were going wrong about Asia.

Asia: UBS Trumps Citi

Hungry for expansion, Switzerland's private banks often misread Asia as an El Dorado. Salem also played up the services for the wealthy that Citi can provide and Swiss banks typically didn't at the time – loans and financing, for example.

Salem, who retired in February, made the comments shortly after UBS pipped Citi as Asia's largest wealth manager. The veteran banker appears willing to fade out that two more Swiss wealth managers – Julius Baer and Credit Suisse – are breathing down Citi's neck on assets under management.

To be sure, Swiss wealth managers can also show their share of bumbled Asian expansion efforts too. But Credit Suisse insiders frequently remark that Citi's private bank only sits as prominent in league tables as it does because the U.S. bank includes a business with less wealthy, or affluent, clientele.

Growth – Across the Board

Charrington, the overall Citi wealth boss, is vindicated by the $42 billion in net new client money that his private bankers hoovered up last year – growth of 17.2 percent. But the statistics illustrate that rivals aren't far behind: UBS netted $44 billion, according to date from Scorpio Partnership, representing growth of 17 percent.

Credit Suisse's $32 billion translates to 18 percent growth, while Julius Baer pipped all its Swiss rivals as well as Citi with $64 billion in new money – a whopping 20 percent growth rate. Hardly the changing of the guard that Charrington hopes to portray.

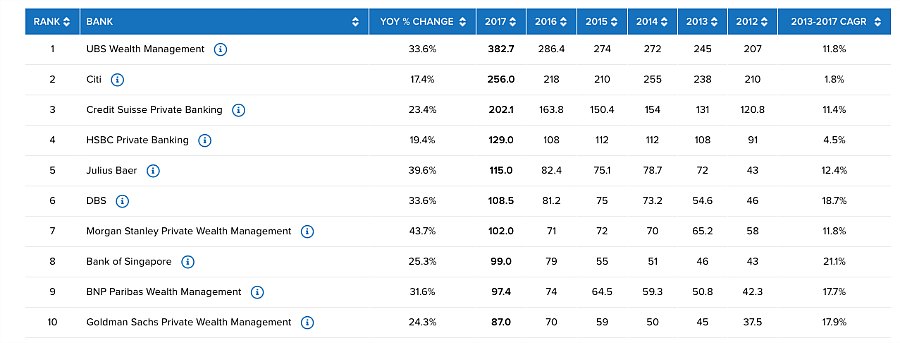

Swiss Champions of Asia

The contrast is especially dramatic in Asia, the hotbed of growth for wealth managers at the moment. Citi may have grown by 17 percent last year, but its average growth in the last five years was a mere 2 percent, according to calculations by trade publication «Asian Private Banker».

Where do the Swiss stand? UBS grew by more than one-third last year, and an average 12 percent since 2013; Credit Suisse by 23 percent and 11 percent respectively, and Julius Baer by 40 percent and 12 percent respectively.

In that sense Charrington's observation that a small group of banks – he includes Citi, J.P. Morgan, Credit Suisse and UBS in this group – are pulling away from the global competition isn't correct.