Banks’ value chains are increasingly spread across multiple supplier industries, so it is no longer possible to track the sector’s performance using simple statistics, Thomas Ruehl from the Swiss Bankers Association.

Thomas Ruehl is head of sectoral analysis at the Swiss Bankers Association

Thomas Ruehl is head of sectoral analysis at the Swiss Bankers Association

There was a time when a bank could house its entire operations in a single building: tellers at the front, administrative offices behind, vault in the basement, opulent client meeting rooms upstairs, archive in the attic. It was relatively easy for outsiders to understand the organization and determine how many people worked for the bank: from the apprentice in the treasury department to the accountant, the teller, and the director, everyone in the building was employed directly by the bank. The entire value chain was located under one roof.

Stark Contrast

This stands in stark contrast to today’s banking sector: value chains are globally organized and more and more dispersed. Banks are increasingly working with third-party companies. As in other organizations, non-core activities such as catering, cleaning and even some IT and other important functions are being outsourced to other companies.

At banks, the scope of this outsourcing is quite broad in some areas and can extend to central services such as processing all payments for individual banks. The industry’s moves to specialize and get to grips with technological change have made this trend more pronounced still.

No Longer Bank Employees

Regulations such as the «too big to fail» legislation require big banks to draw up plans for resolution in the event of bankruptcy. Predetermined break-up points such as hiving off infrastructure into specially established service companies can minimize collateral damage in such a scenario.

These companies are often subsidiaries that work exclusively for the parent company. Employees enter and exit the same building as before, just like their colleagues who remain employed by the bank. They perform the same tasks as before the changeover but – at least on paper – are no longer bank employees.

Production Remains Swiss-Based

From a macroeconomic perspective, this effect alone has hardly changed anything. In the statistics, however, these outsourced jobs and their value-added are no longer attributed to banks but to other sectors such as management consultancy, call centers, IT or other services.

What counts for Switzerland’s economic success are the services in demand and the efficiency of their delivery, as well as the fact that production remains Swiss-based.

Hard to Believe

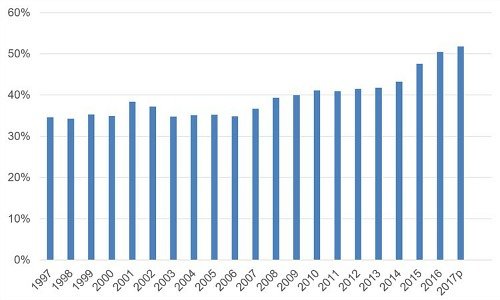

The input ratio, i.e. the share of production value that third-party companies generate for banks, rose markedly from 42 percent to 52 percent in just three years between 2013 and 2015.

According to federal statistical data, employment at the big banks fell by 9,850 full-time equivalents from 2016 to 2017, while employment at management consulting firms – you might find it hard to believe – rose by exactly the same number. Did the statisticians simply shift these people en masse to another industry?

Staff Levels at the Banks in Switzerland (Domestic)

(Source: SNB Banking Barometer, SNB)

The fact that the figures are an exact match is probably just a coincidence. However, what is important here is the statistical effect caused by some of these people no longer qualifying as bank employees but instead being allocated to a different industry. These individuals no longer appear in the bank statistics, although this has little influence on economic reality.

Structural Transformation

This shows that the banks’ value chain is increasingly distributed across supplier industries and also that statistics have their pitfalls. A single figure, such as the number of people employed by the big banks, is often not enough to understand how an entire industry is performing.

The structural transformation underway among banks in Switzerland is old news, and it is true that this transformation will improve the sector’s viability going forward. However, the idea that it is as massive as a quick look at the employment figures would suggest is clearly wrong.

Despite the uncertain environment, the adjustment process and the economic challenges, Switzerland’s banks are on a solid footing. Assets under management are rising thanks to net new money, and not just thanks to the tailwinds provided by buoyant financial markets. Earnings are also increasing – not to the same extent as before the financial crisis, but more sustainably.

Banks’ Input Ratio Rising

(Source: FSO, production account)