In recent years, digital assets such as Bitcoin and other cryptocurrencies have become increasingly relevant, which is also reflected in the fact that renowned innovative companies such as Tesla also invest in Bitcoin. However, not only Bitcoin alone but also a combination of a wide variety of cryptocurrencies in the form of a Crypto Index can represent a smart diversification of a portfolio not correlated with traditional asset classes.

By Roger Darin, Advisor Digital Assets, InCore Bank

One thing seems dear by now: Bitcoin and digital assets will remain in the future. In the past year, for example, publicly traded companies such as MicroStrategy and Tesla have invested significant amounts in Bitcoin. Meanwhile, EI Salvador became the first nation-state, declaring Bitcoin legal tender in September 2021.

Since then, the Latin American state has invested in Bitcoin in several episodes. While MicroStrategy, Tesla or El Salvador are among the most illustrious Bitcoin investors, they are only the tip of an ever-growing iceberg. More and more investors – from retail investors to institutional players – are entering the digital asset market.

This fact is reflected by the remarkable increase in the total market capitalization of all cryptocurrencies: at the beginning of 2021, the market valuation was approximately $763 billion. Shortly before the end of 2021, the market capitalization of all cryptocurrencies more than tripled, and in November 2021 it even scratched the $3 trillion mark in the meantime.

A New (Alternative) Asset Class

For a growing number of investors, cryptocurrencies and digital assets have long since become an asset class in their own right. According to professional market analysts, they are to be placed alongside art, hedge funds or commodities among alternative investments. Among cryptocurrencies, Bitcoin still stands out.

As the figures impressively show, Bitcoin was the best performing asset of the past decade. Still the most prominent cryptocurrency, it accounts for around 40 percent of the total market capitalization of this new asset class. This fact is also due to the diversity of Bitcoin investment products. For example, the first bitcoin futures ETFs were launched in the US in the last quarter of 2021.

Bitcoin: a Smart Portfolio Diversifier

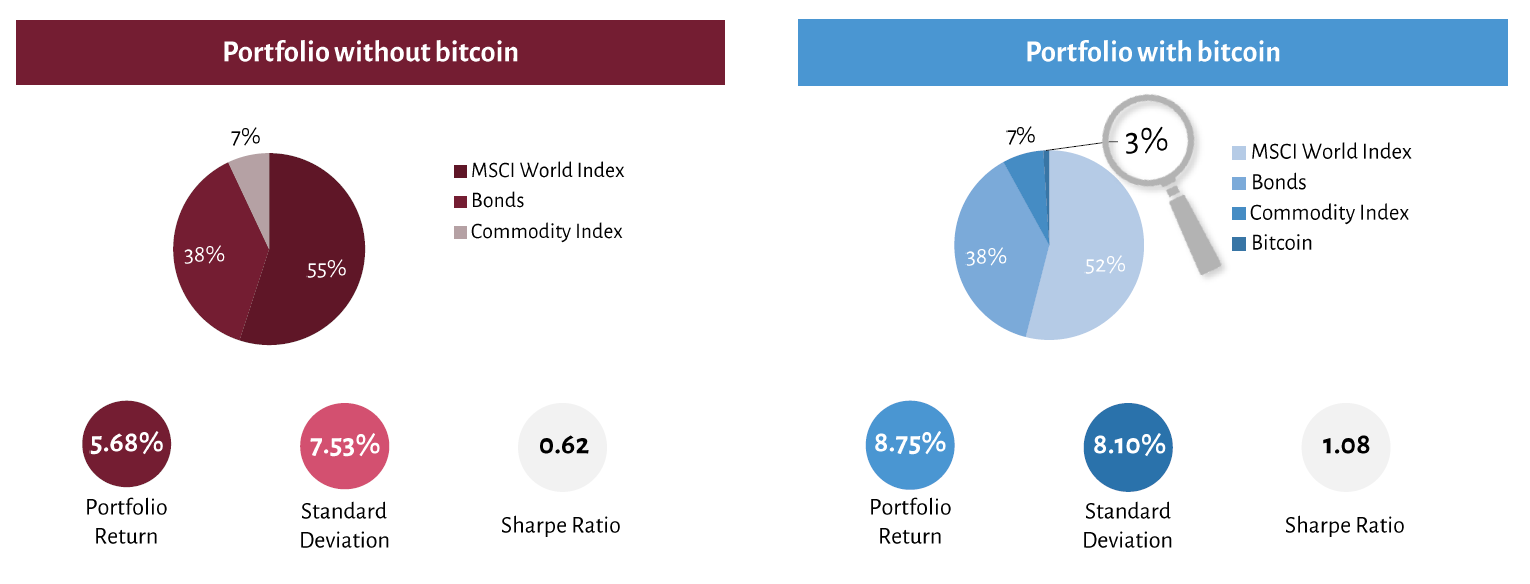

The impressive performance of digital assets over the past years can also be put into a portfolio context. The portfolio comparison for portfolios with and without bitcoin allocation shows that relevant portfolio parameters improve with a bitcoin allocation.

This can be illustrated by a concrete example of a classic portfolio1. This contains 55 percent equities (MSCI World Index), 38 percent bonds (TIPS Bond ETF) and 7 percent commodities (Invesco DB Commodity ITF). For the period from 2015 to 2021, this diversified portfolio has generated an annual return of 5.68 percent with a standard deviation (volatility) of 7.53 percent.

(Source: InCore Bank)

Adding only 3 percent Bitcoin at the expense of the equity portion, which itself performed well, has a positive effect on the portfolio. Thus, the performance of the portfolio could be increased to an annual return of 8.75 percent thanks to Bitcoin allocation, while the standard deviation increased only minimally to 8.10 percent.

This positive effect of Bitcoin is also reflected in the change of the Sharpe Ratio, a commonly used portfolio metric to show the risk-adjusted return.

A high Sharpe ratio indicates that high performance has been achieved with relatively low risk. The higher the Sharpe ratio for a selected portfolio compared with a benchmark portfolio, the better the risk/return ratio of the former compared with the latter.

For the selected example, the Sharpe Ratio for the classic portfolio without Bitcoin addition is 0.62. The addition of Bitcoin increases the Sharpe Ratio to 1.08. This fact allows the following conclusion: Bitcoin correlates little with conventional asset classes and represents a reasonable diversification of a classic portfolio.

Other Digital Assets – Same Effect

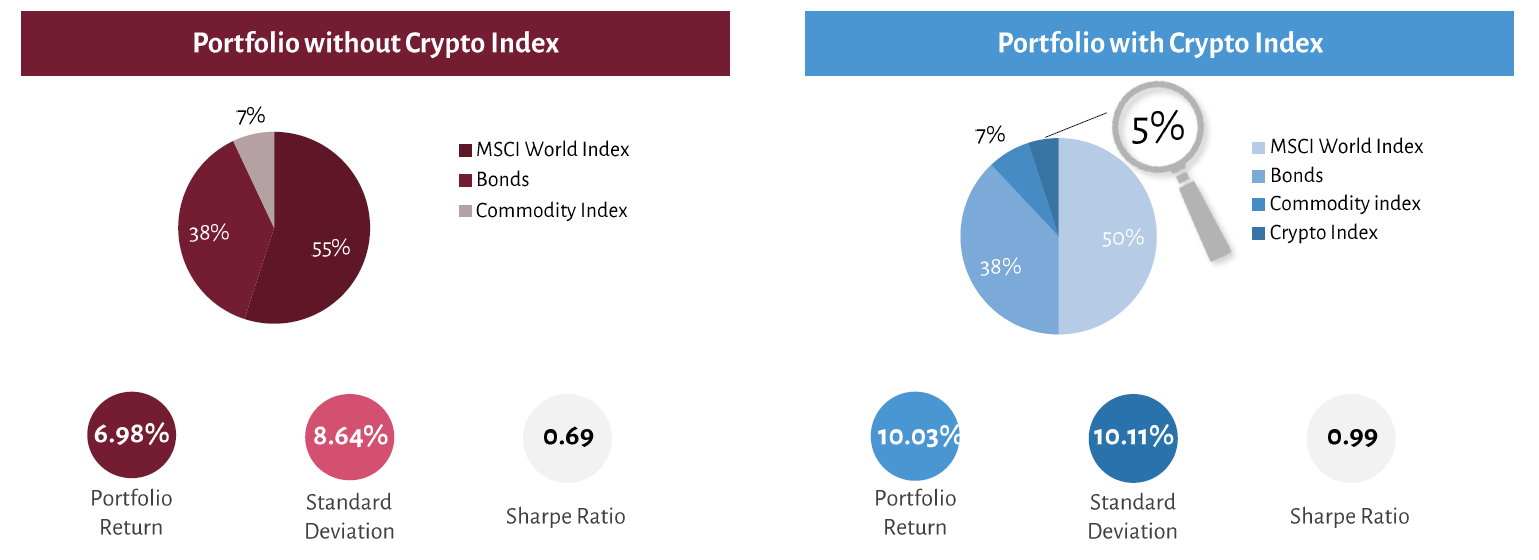

In the meantime, there are countless other cryptocurrencies that also commonly fall under the term digital assets. Some of them have now reached a considerable market capitalization and are therefore also taken seriously by professional investors. The same classic portfolio2 can also be compared to a portfolio that has been supplemented with a combination of different cryptocurrencies.

Cryptocurrencies that can be found among the top ten in terms of market capitalization were selected and combined to form a Crypto Index. This is composed as follows: 5 percent Bitcoin (BTC), 5 percent Bitcoin Cash (BCH), 10 percent Ether (ETH), 40 percent Cardano (ADA) and 40 percent Ripple (XRP).

Together, these cryptocurrencies make up 5 percent of the total portfolio, which are included in the portfolio instead of stocks. Due to the younger age of these cryptocurrencies compared to Bitcoin, a more recent and therefore shorter time period of 2018 to 2021 was considered.

The classic portfolio without crypto allocation achieved a return of 6.98 percent with a standard deviation of 8.64 percent during this period. By adding the selected cryptocurrencies, the performance increased from 10.11 percent to 10.03 percent with a standard deviation during the same period.

Likewise, the Sharpe Ratio changes from 0.69 to 0.99. Thus, this example shows: Not only Bitcoin alone but also a combination of various cryptocurrencies in the form of a Crypto Index can represent a meaningful diversification of a portfolio.

(Source: InCore Bank)

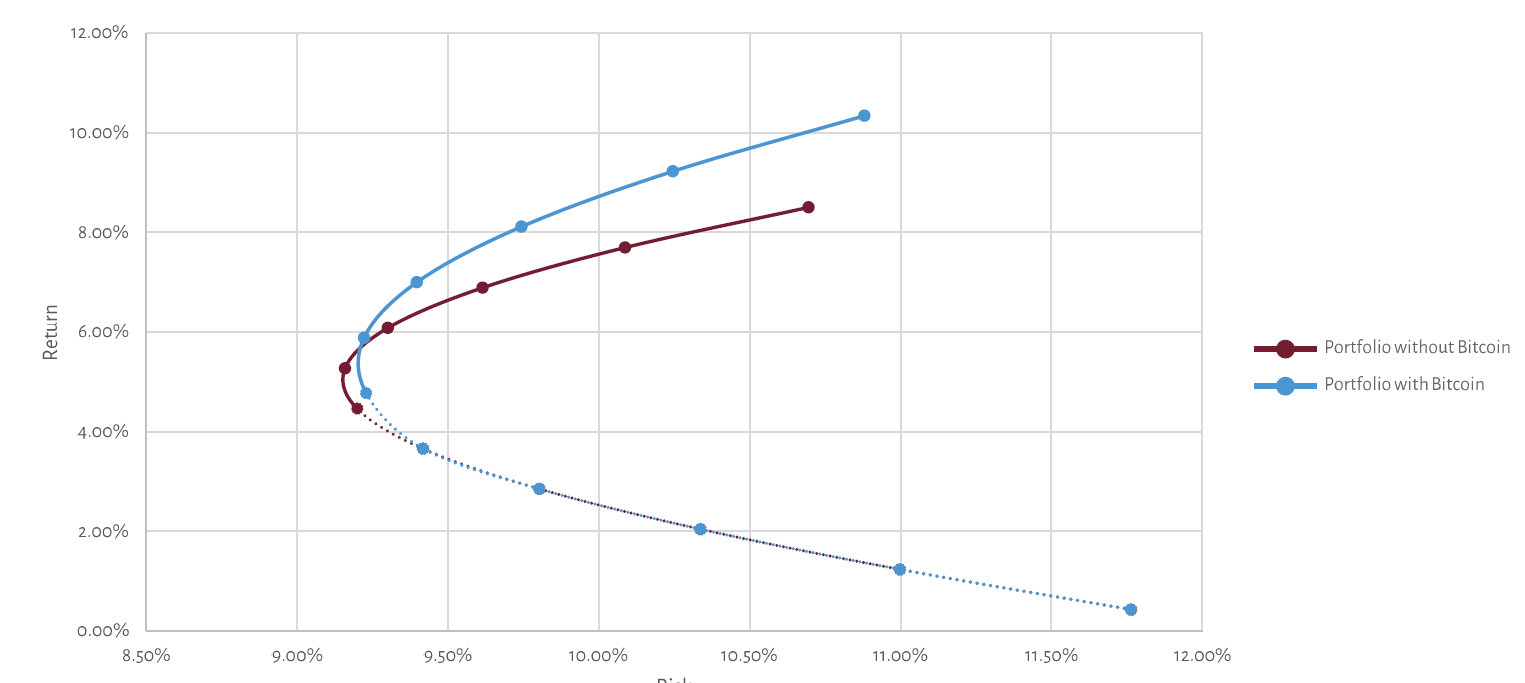

A Shift in the Efficiency Curve

The advantage of adding cryptocurrencies is also illustrated by the so-called efficiency curve. This shows the highest possible return and the greatest risk that different portfolio allocations can have. Since the return is shown on the Y-axis and the risk on the X-axis, a shift of the efficiency curve upwards meant that a higher return can be achieved for a corresponding portfolio with the same risk.

Such an upward shift of the efficiency curve results for those portfolios3 to which digital assets have been allocated as an add-on.

(Source: InCore Bank)

In other words, at the same level of risk, adding cryptocurrencies can achieve a higher return – or adding them at the same level of return can lower the risk.

Relevant for the Future?

Given these findings from portfolio theory, the question arises: Will the positive effect of an admixture of cryptocurrencies be able to hold up in the future? It is a well-known fact that collected data is always from the past and does not provide guaranteed statements about the future.

Looking in the rearview mirror makes performance and the risk-return ratio appear positive. However, why should portfolio findings apply in the immediate future? In Bitcoin's favor is its progressive establishment as digital gold. Bitcoin's promise of scarcity has held over the past twelve years, and with each additional year that it holds, it solidifies in the minds of an ever-increasing number of people.

Bitcoin's strength as an investment becomes particularly clear when other asset classes are put in relation to the central banks' money supply expansion. For example, comparing the S&P soo not to its dollar valuation, but to the Fed balance sheet, shows that the price increases are due to a strong expansion of the money supply.

If one chooses the correct denominator-the central bank balance sheet, that is- prices are flat. Over the past decade, the S&P 500 has grown nominally by an average of 15 percent per year. Interestingly, this is pretty much in line with the annual expansion of the U.S. Federal Reserve balance sheet.

As a kind of hedge against perpetual monetary expansion by central banks, Bitcoin and other cryptocurrencies are likely to continue to find favor in the near future. The end of the acceptance curve is likely to be far from reach. If cryptocurrencies continue their triumphant march, Bitcoin and other digital assets will also prove tobe a smart, non-correlated diversification for a portfolio in the near future.

1, 2, 3 These are sample portfolios. All information without liability.

Roger Darin is Advisor Digital Assets at InCore Bank. The Blockchain and Digital Assets topic is the ideal field of activity for the trained banker, who has always been driven by his interest in technology. In addition to his professional activities, he teaches on these topics at various Swiss schools and universities. He is also a community manager on the board of the Bitcoin Association Switzerland.