Banks and asset managers lending in parallel could offer investors an interesting credit solution.

By Gianluca Oricchio, CEO of Muzinich & Co. SGR and Global Head of Artificial Intelligence Solutions

Over the last 15 years, banks have focused on de-risking while asset managers step in to fill the lending gap (so-called Alternative Lending). However, we have seen the recent emergence of Parallel Lending where asset managers lend to companies alongside banks.

Under Basel Regulations, banks can optimize their net return/risk-weighted asset ratios by sharing plain vanilla term loans with asset managers who lend under the same loan agreement and maintain 100 percent of the capital-light business generated by the invested company.

This banking business model is defined as Originate-and-Share (where the banks remain co-invested) as opposed to the Originate-and-Distribute (where the banks have no skin in the game).

Potential Win-Win Scenario

This approach may benefit both parties. The bank can reduce risk and counterparty exposure while providing the asset manager access to its distribution network and a large number of sourced transactions. The asset manager may then seek to build well-diversified portfolios, benefiting from cash buffer provided by the bank’s revolving credit facilities/short-term financial support in the event of temporary stress.

Globally, the potential market is around $96.2 trillion1, while in Europe it is around 4.9 trillion euros 2.

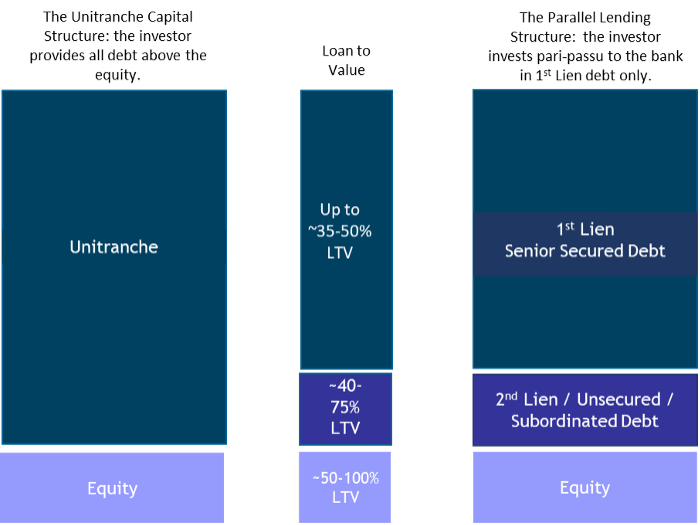

Illustrative First Lien Loan in the Company Capital Structure

(Source: Goldman Sachs Asset Management Private Credit, Senior Direct Lending Platform, April 2022, (pg. 11). For illustrative purposes only. Click graphic to enlarge)

A parallel lending investment strategy primarily invests in first lien/club loans and senior secured assets which may be the safest/most senior and often secured assets. A well-diversified and granular portfolio (minimum circa 100 loans) may protect capital while maximizing yield by capitalizing on the minimization of black swan events through diversification, and on the premise that joint default probabilities are lower than the default probability of a single holding.

Given this focus on risk reduction, a portfolio can potentially be rated investment grade (IG), enabling banks to provide long-term leverage to the portfolio at very competitive interest rates. However, an asset manager must be fully independent of a bank yet have direct access to any company under consideration for lending to carry out the due diligence process, and must have the same quantitative tools as European banks (i.e., Basel III Advanced Internal Credit Rating Models).

Use of Artificial Intelligence

We advocate an investment process with three pillars to include qualitative/fundamental analysis, Basel III Advanced Internal Credit Rating Models (and risk-adjusted pricing tools) and new artificial intelligence (AI)/deep learning critical decision support systems (or advanced risk tools).

AI should be used to enhance decision-making through augmented data analysis of enormous sample size, and not, in its own right, an algorithmic or «black box» credit selector. A multi-layer neural network is a powerful tool for data analysis where AI combines with human analysis to increase the accuracy and quality of output and aims to increase the ability to separate bad companies from good during a due diligence process.

However, the final investment decision remains human-based. Looking ahead, we expect to see an increase in credit funds based on parallel lending because they may offer attractive returns, low volatility (they do not have a daily mark to market) and low interest rate risk because most of the loans are floating rates.

This is against a backdrop of ongoing bank deleveraging where there is an abundant supply of loans – especially in the underserved lower middle market – capital protection for banks and innovative credit analysis where there is a vast, under-mined universe of credit data on small and medium-sized enterprises.

In an environment dominated by recession and inflation, we believe a well-diversified portfolio of floating rate senior credit, as well as low-leveraged invested companies (lev=3x), have broad appeal.

1Financial Stability Board report. Non-Bank Financial Intermediation Report, December 2021. Most recent data used.

2ECB: Statistical Data Warehouse, as of January 2022. Most recent data used.

Gianluca Oricchio is CEO of Muzinich & Co. SGR and Global Head of Artificial Intelligence and Robotics. Prior to joining Muzinich, Gianluca has been Managing Director in several European Banking Groups and has developed SME Credit Rating Models and Early Warning Systems. He has been an advisor of Moody’s Analytics. Gianluca is a Ph.D. in International Accounting and a Full Professor of Corporate Finance and Accounting. He graduated from La Sapienza University.

Muzinich & Co. referenced herein is defined as Muzinich & Co., Inc. and its affiliates. This material has been produced for information purposes only and as such the views contained herein are not to be taken as investment advice. Opinions are as of date of publication and are subject to change without reference or notification to you. Past performance is not a reliable indicator of current or future results and should not be the sole factor of consideration when selecting a product or strategy. The value of investments and the income from them may fall as well as rise and is not guaranteed and investors may not get back the full amount invested. Rates of exchange may cause the value of investments to rise or fall. Emerging Markets may be more risky than more developed markets for a variety of reasons, including but not limited to, increased political, social and economic instability; heightened pricing volatility and reduced market liquidity. Any research in this document has been obtained and may have been acted on by Muzinich for its own purpose. The results of such research are being made available for information purposes and no assurances are made as to their accuracy. Opinions and statements of financial market trends that are based on market conditions constitute our judgment and this judgment may prove to be wrong. The views and opinions expressed should not be construed as an offer to buy or sell or invitation to engage in any investment activity, they are for information purposes only. This document contains forward-looking statements, which give current expectations of future activities and future performance. Any or all forward-looking statements in this document may turn out to be incorrect. They can be affected by inaccurate assumptions or by known or unknown risks and uncertainties. Although the assumptions underlying the forward-looking statements contained herein are believed to be reasonable, any of the assumptions could be inaccurate and, therefore, there can be no assurances that the forward-looking statements included in this discussion material will prove to be accurate. In light of the significant uncertainties inherent in the forward-looking statements included herein, the inclusion of such information should not be regarded as a representation that the objectives and plans discussed herein will be achieved. Further, no person undertakes any obligation to revise such forward-looking statements to reflect events or circumstances after the date hereof or to reflect the occurrence of unanticipated events. Issued in the European Union by Muzinich & Co. (Ireland) Limited, which is authorized and regulated by the Central Bank of Ireland. Issued in Switzerland by Muzinich & Co. (Switzerland) AG. Registered in Switzerland No. CHE-389.422.108. Registered address: Tödistrasse 5, 8002 Zurich, Switzerland.

2023-03-20-10525