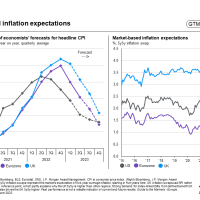

Although overall inflation is expected to continue to fall in the coming months, experts at J.P. Morgan Asset Management anticipate stronger inflationary fluctuations as the global economy enters a phase in which shortages of key commodities become more present and problematic. Read more in the latest «Guide to the Markets».

J.P. Morgan Asset Management’s «Guide to the Markets» provides client advisors and professional investors with targeted support for making the best investment decisions.

Too Good to be True

Markets have become increasingly optimistic that inflationary pressures will recede even if economic activity remains robust (Guide to the Markets – Europe page 7). This expectation that Goldilocks will return has buoyed both stock and bond prices this year (pages 48, 72), but such a benign scenario seems too good to be true.

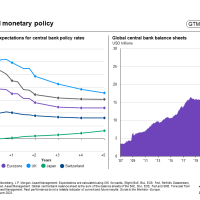

We expect the central banks will need to maintain their foot on the brake to drive away excess inflation (page 9). A recession is still our base case.

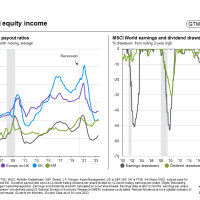

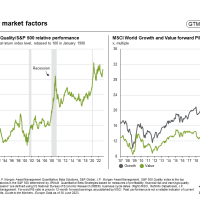

Boost Resilience

Given the recent rally, neither equity nor credit markets appear priced for a period of economic weakness. Against this backdrop, we believe that investors should focus on high-quality credit (page 70) and look to boost the resilience of an equity portfolio via exposure to strong balance sheets, resilient dividend payers and regional diversification (pages 48, 51, 53).

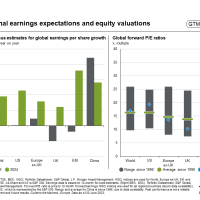

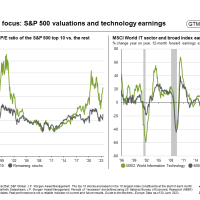

We caution against having too much confidence that large-cap tech will prove defensive in an earnings recession (page 65).

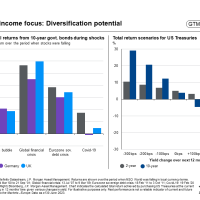

Think More Broadly About Diversification

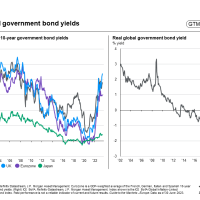

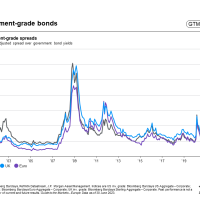

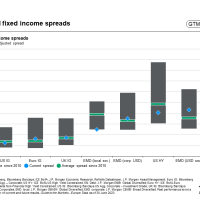

Real yields in core government bonds are more attractive than they have been in over a decade (page 68). If a recession is accompanied by a quick dissolution of inflationary pressures, core bonds will provide ballast to a portfolio (page 73). But 2022 is a reminder that inflation is not dead and can be extremely damaging to the price of stocks and bonds.

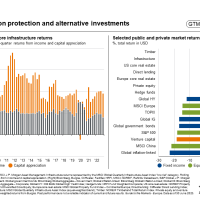

Alternatives are needed to insulate a portfolio from inflation shocks (page 78).

From Abundance to Scarcity

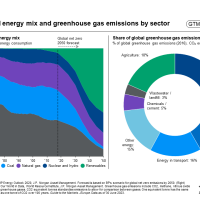

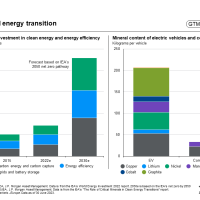

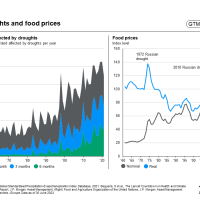

Although headline inflation will fall further in the coming months, we do expect more inflation volatility as the global economy enters a period in which scarcity of key commodities becomes more apparent and problematic. Our key concerns center on low-carbon energy, materials, food and water, and labor markets (pages 16, 83, 84, 86).