Recent geopolitical and economic events have brought an inflection point in global financial markets. Experts at J.P. Morgan Asset Management analyze the latest data to assess the situation and forecast the outlook for the next six months.

J.P. Morgan Asset Management’s «Guide to the Markets» provides client advisors and professional investors with targeted support for making the best investment decisions.

The charts and tables provide a quick and uncomplicated overview. The latest «Guide to the Markets» covers the following topics, and more:

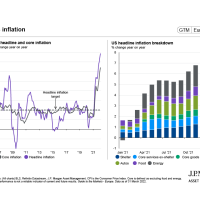

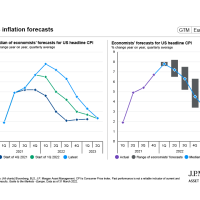

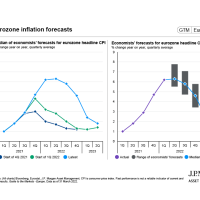

1. Inflation to be Higher for Longer

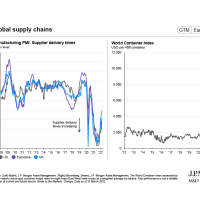

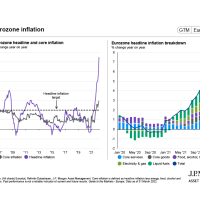

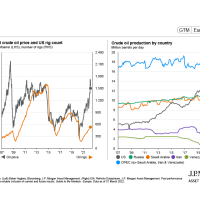

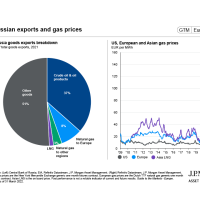

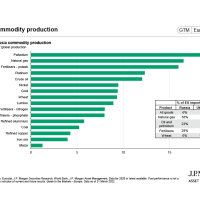

The Ukraine crisis has resulted in a sharp increase in the price of many commodities (Guide to the Markets – Europe pages 76-79). Alongside this, supply bottlenecks are likely to persist as China imposes lockdowns to control the spread of Covid-19 (page 13).

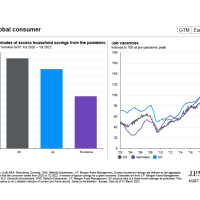

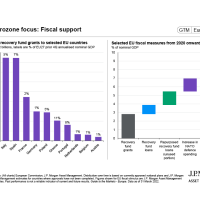

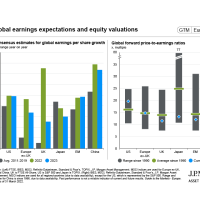

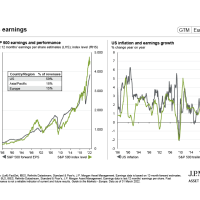

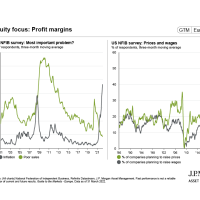

Inflation is likely to be higher for longer (pages 23, 24, 32, 33). This will weigh on disposable consumer incomes (pages 20 & 40) and corporate profits (page 66), although we expect governments to provide some fiscal support to ease the pressure (page 36).

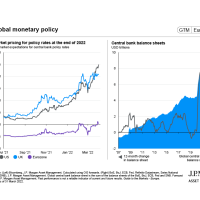

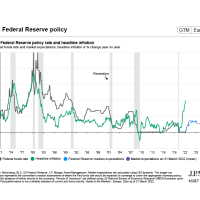

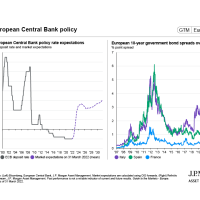

2. Interest Rates to Keep Rising as Long as Growth is Robust

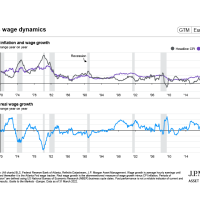

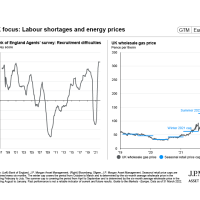

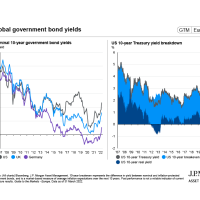

With labour markets tight in both the US and UK (page 11), central banks are concerned that cost shocks will feed into higher wages and inflation will become more entrenched. The Federal Reserve has signalled its intention to deliver multiple rate hikes over the course of this year (pages 9 & 25).

As long as the recovery remains robust, we expect these to be delivered and for longer-term interest rates to rise further. The European Central Bank is expected to be more patient (page 34), particularly in the event of a more severe disruption to European oil and gas supplies from Russia.

3. Higher Interest Rates Will Help Value Stocks Catch up

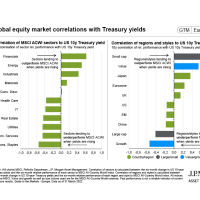

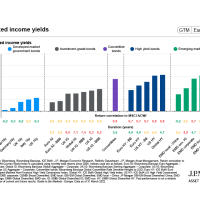

Persistently higher inflation is likely to pose ongoing challenges for government bonds and high-quality fixed income (page 68). Although interest rates are expected to rise, we expect real interest rates to remain negative for some time (page 69).

Equities should be resilient to higher interest rates as long as corporate earnings continue to grow (pages 49 & 55), although value stocks are likely to benefit from persistent inflation and higher interest rates more than growth stocks (page 50).