What do the shares of Switzerland’s central bank have in common with bitcoin? Both are subject to huge speculative bubbles. There may be tears, entrepreneur Adriano Lucatelli warns in an exclusive essay for finews.first.

finews.first is a forum for renowned authors specialized on economic and financial topics. The texts are published in both German and English. The publishers of finews.com are responsible for the selection.

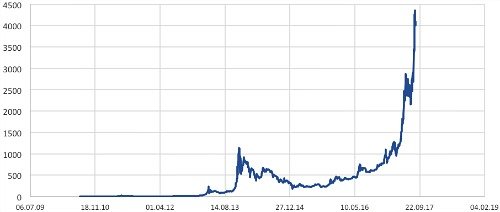

Bitcoin, the digital currency, is the current top seller: it climbs to a new high nearly on a daily basis as more and more investors looking for the quick buck jump on the bandwagon as it gathers speed.

Similarly, the listed share of the Swiss National Bank (SNB) are going through the roof, going from record to record. What is going on here? What do the two securities have in common? Are we looking at two speculative bubbles developing? The answer is yes.

«The market doesn't make mistakes»

Eugene Fama said there are no financial market bubbles. He is the founder of the efficient market hypothesis and winner of the Nobel Prize in Economic Sciences of 2013. According to the economist, markets in principal are efficient and market prices a reflection of every available piece of information.

The market thus doesn’t make mistakes and records are the result of an efficient pricing mechanism. So far, so good. Indeed, it wouldn’t be hard to find good reasons for the rapid increase in valuations: Chinese and Venezuelans want to take their money abroad to safety and flock to bitcoin.

«Bubbles when small investors buy with wild growth fantasies»

Robert Shiller, who received a Nobel Prize in the same year as Fama, vehemently disputed the hypothesis about the efficient market. In fact, speculative bubbles occur regularly citing the dotcom crash and the most recent financial crisis. The Yale economist says that bubbles are a subtle phenomenon of social psychology, developing when small investors are buying assets with wild growth phantasies – in the hope of making a quick profit.

This group tends to jump on the bandwagon at a late stage and add further fuel to the fire shortly before the turning point has been reached – in other words, at a time when it is too late. This phenomenon – the proverbial shoe shine boy talking stocks – is the latest stage of the development of a bubble when badly-informed private investors buy securities at exaggerated levels.

«Bubbles only develop when it is impossible to hedge»

Both Nobel Prize winners are right. Bubbles only develop when it is impossible to hedge cheaply and efficiently, or by betting against further increases through short selling. The free price setting on the market isn’t possible without short selling, because nobody can confront the increase by selling assets. And that’s the case here: hedging and short selling are very expensive if not impossible in the case of both bitcoin and the SNB's stock.

The current situation reminds us about the Hollywood film «Big Short». Many investors in the film knew that a majority of collateralized debt obligations were bad. And yet it was impossible to bet on a fall in prices. That’s why Michael Burry, the eccentric hedge fund manager, was able to bet on the predictable crash with an instrument created solely for his purposes – an option not available to small investors.

Bitcoin / Dollar

(Source: Bloomberg)

What does this mean for private investors who own bitcoin or SNB shares or even both? Quite simply: sell! It can’t be ruled out that bitcoin will rise much further. A factor in favor of a further appreciation is the limitation of production to 21 million units.

And yet, a bitcoin investment is an absolute no-go for investors who do not think long term and can’t take a big (temporary) loss. In the case of the SNB share, it is almost reckless to take part. The stock in essence isn’t much else than a long-term government bond. The dividend has been fixed at a maximum 6 percent of equity or 15 francs a share – regardless of the SNB profit.

Swiss National Bank

(Source: Bloomberg)

Even if everything looks rosy now, the turning point could come at any moment. Or as the late MIT Professor Rudi Dornbusch used to say: «For the crisis to come it takes much longer than you thought, and when it comes, it goes much quicker, than you thought.» If you don’t act now, it might be too late and you could be in for a tearful experience.

Adriano B. Lucatelli is a Swiss businessman, lecturer at University of Zurich and co-founder of Descartes Finance, an independent robo-adviser. He studied economics and international relations at University of Nevada (BA) and at the London School of Economics (MSc). He wrote a PhD at University of Zurich on the global financial market supervision. He started his professional career in 1994 at Credit Suisse and later at UBS, where he worked in various managerial positions both in Switzerland and abroad.

Previous contributions: Rudi Bogni, Peter Kurer, Oliver Berger, Rolf Banz, Dieter Ruloff, Samuel Gerber, Werner Vogt, Walter Wittmann, Alfred Mettler, Peter Hody, Robert Holzach, Craig Murray, David Zollinger, Arthur Bolliger, Beat Kappeler, Chris Rowe, Stefan Gerlach, Marc Lussy, Nuno Fernandes, Beat Wittmann, Richard Egger, Maurice Pedergnana, Marco Bargel, Steve Hanke, Andreas Britt, Urs Schoettli, Ursula Finsterwald, Stefan Kreuzkamp, Katharina Bart, Oliver Bussmann, Michael Benz, Peter Hody, Albert Steck, Andreas Britt, Martin Dahinden, Thomas Fedier, Alfred Mettler, Brigitte Strebel, Peter Hody, Mirjam Staub-Bisang, Adriano B. Lucatelli, Nicolas Roth, Thorsten Polleit, Kim Iskyan, Stephen Dover, Denise Kenyon-Rouvinez, Christian Dreyer, Peter Kurer, Kinan Khadam-Al-Jame, Robert Hemmi, Claude Baumann, Anton Affentranger, Yves Mirabaud, Katharina Bart, Frédéric Papp, Hans-Martin Kraus, Gerard Guerdat, Didier Saint-Georges, Mario Bassi, Stephen Thariyan, Dan Steinbock, Rino Borini, Bert Flossbach, Michael Hasenstab, Guido Schilling, Werner E. Rutsch and Dorte Bech Vizard.